task-gdpval-1

Prompt

Reference Files (37)

Download all (.zip){kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

expert_contributed — Author-generated; mirrors an internal email/correspondence thread used as judgmental audit evidence.

{kind=link}

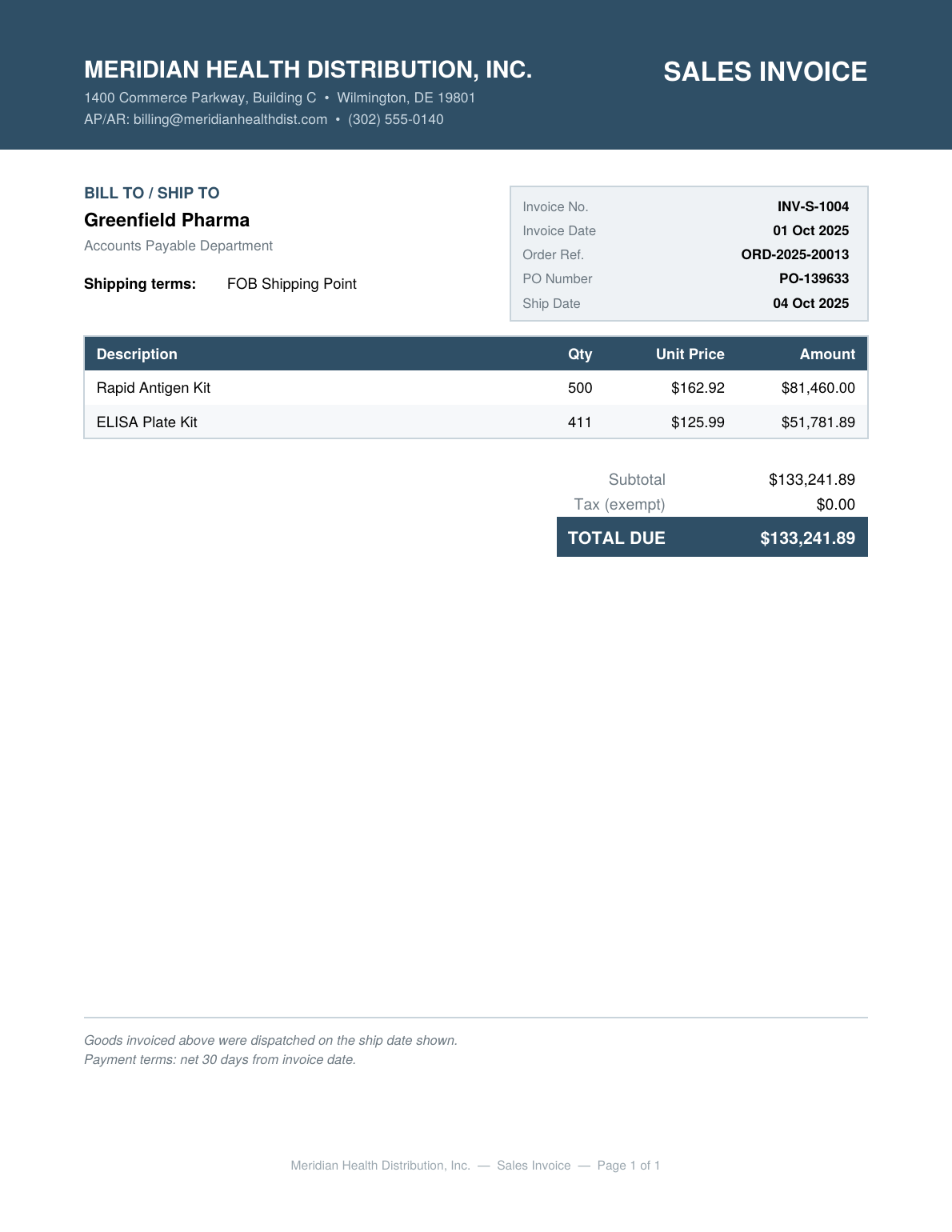

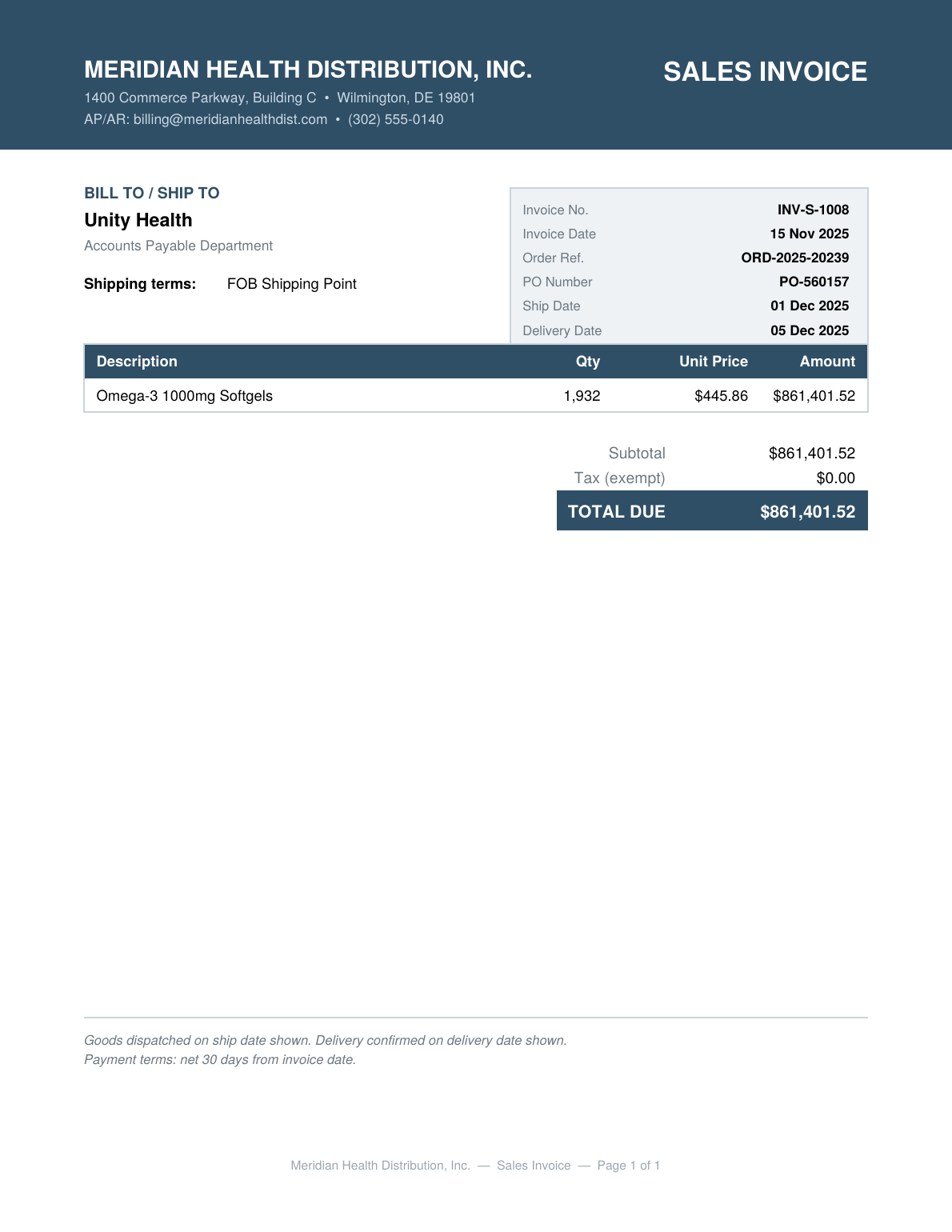

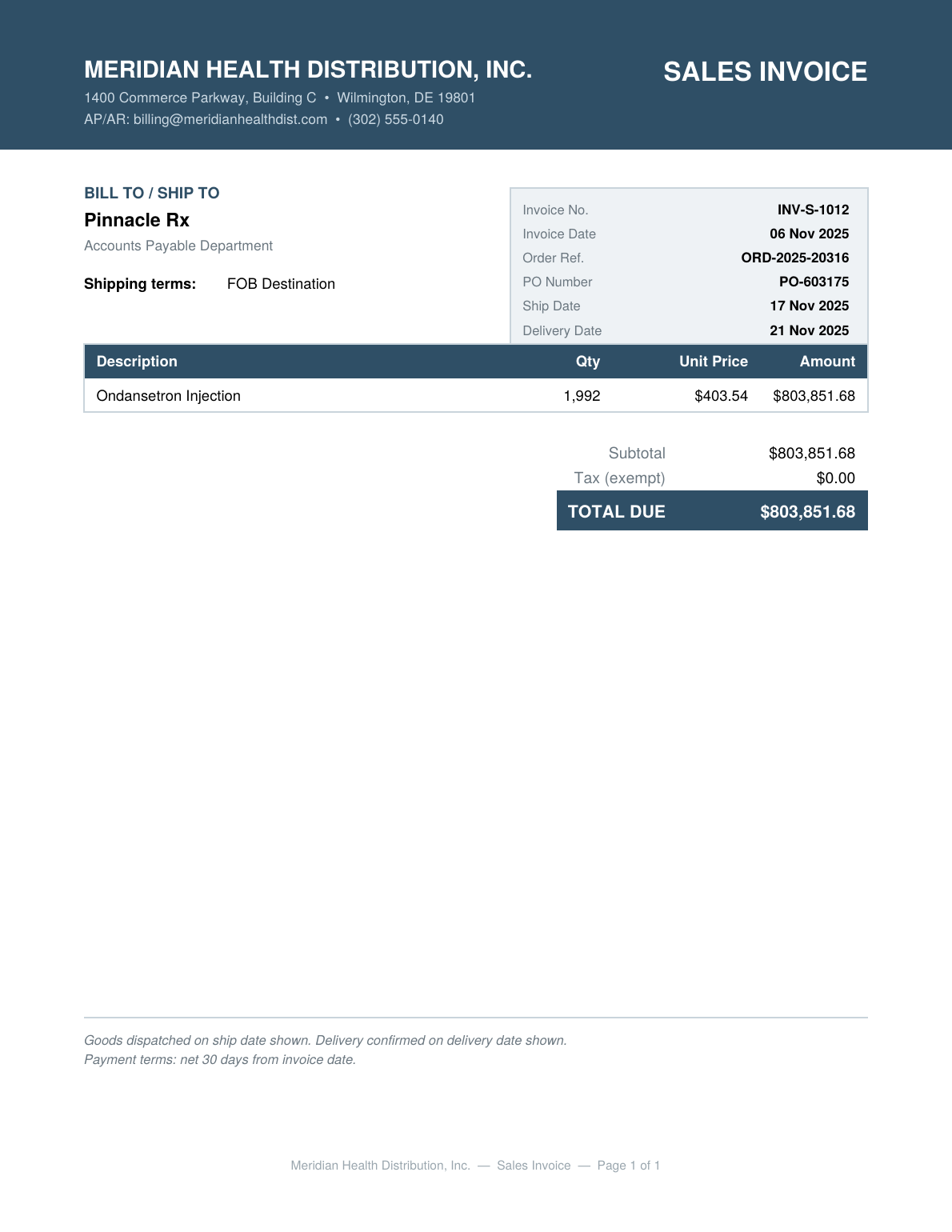

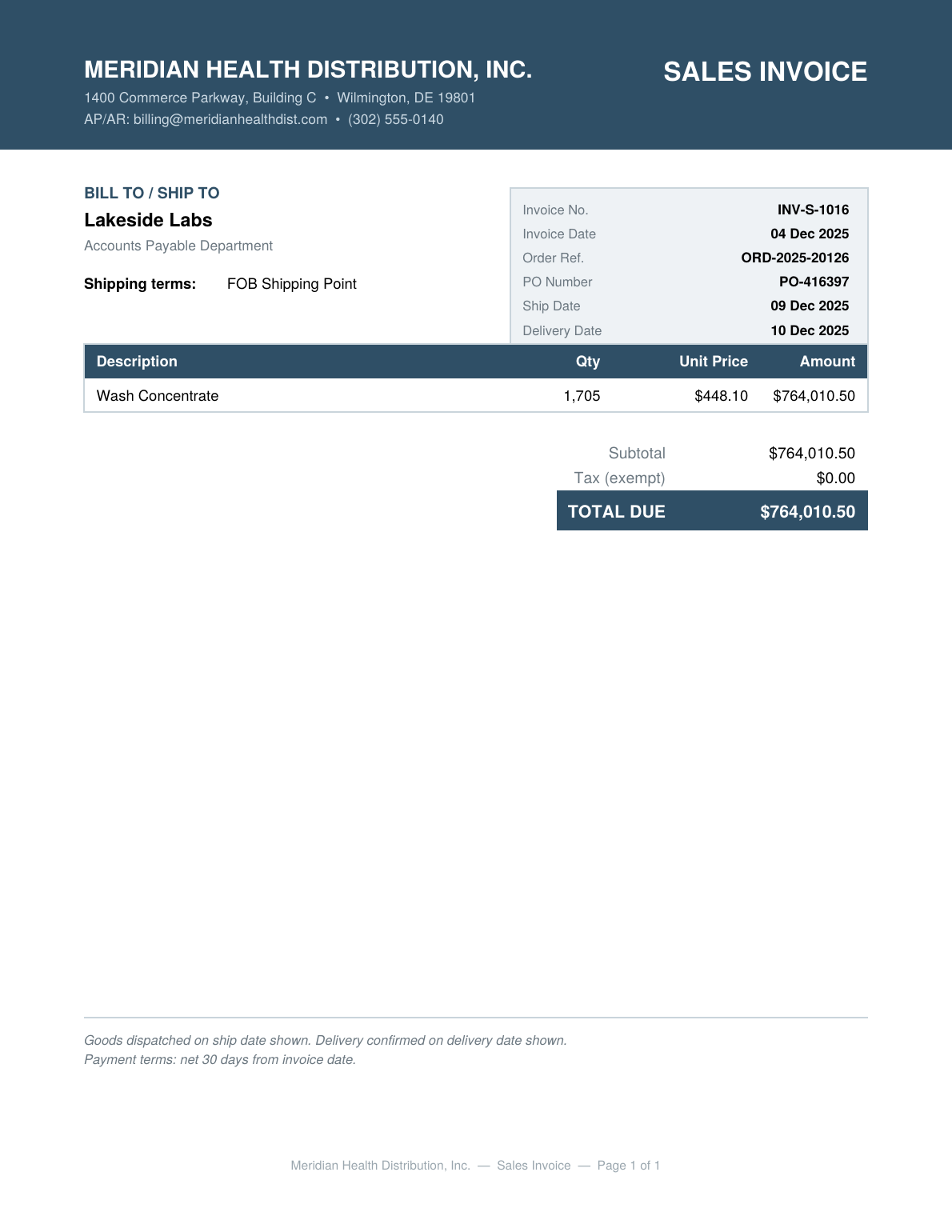

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

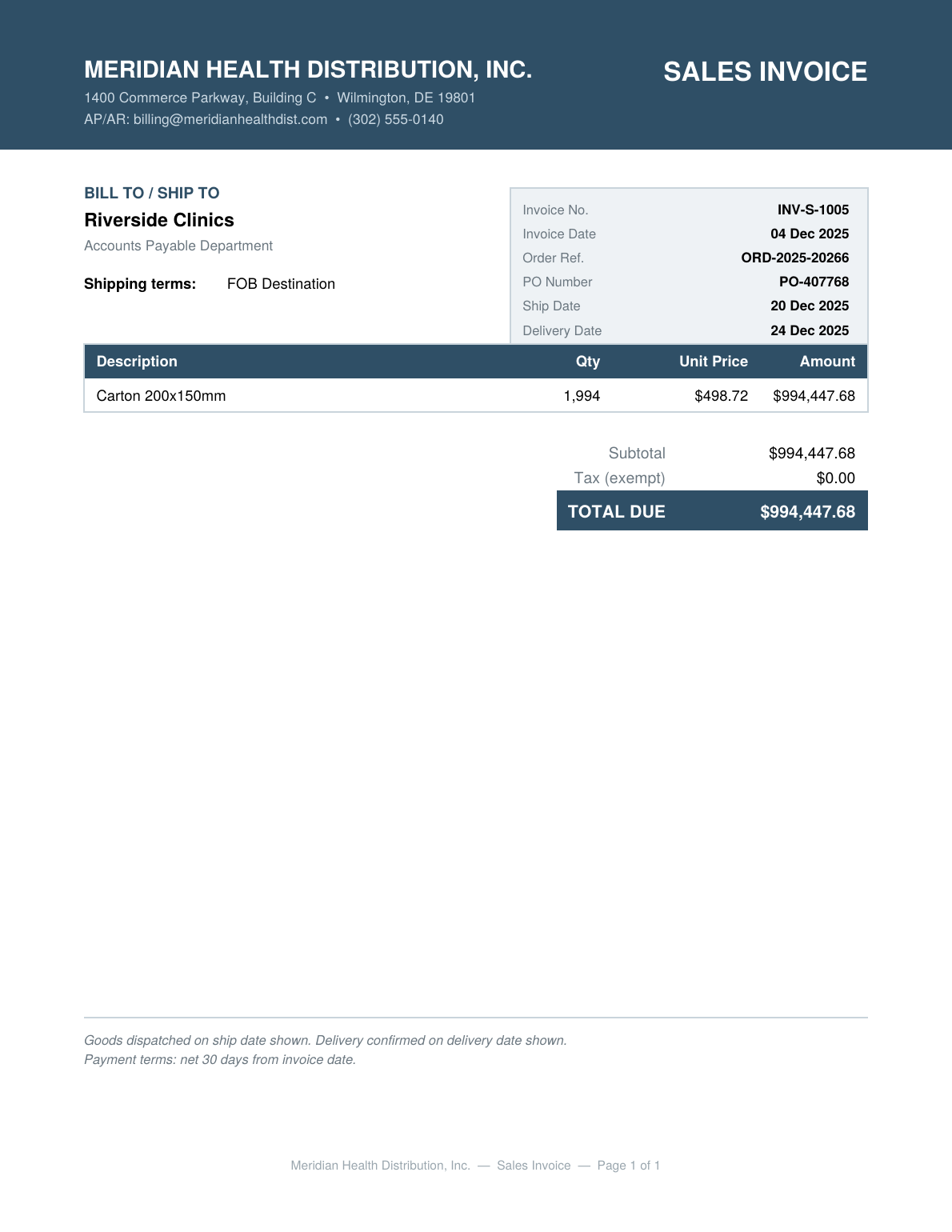

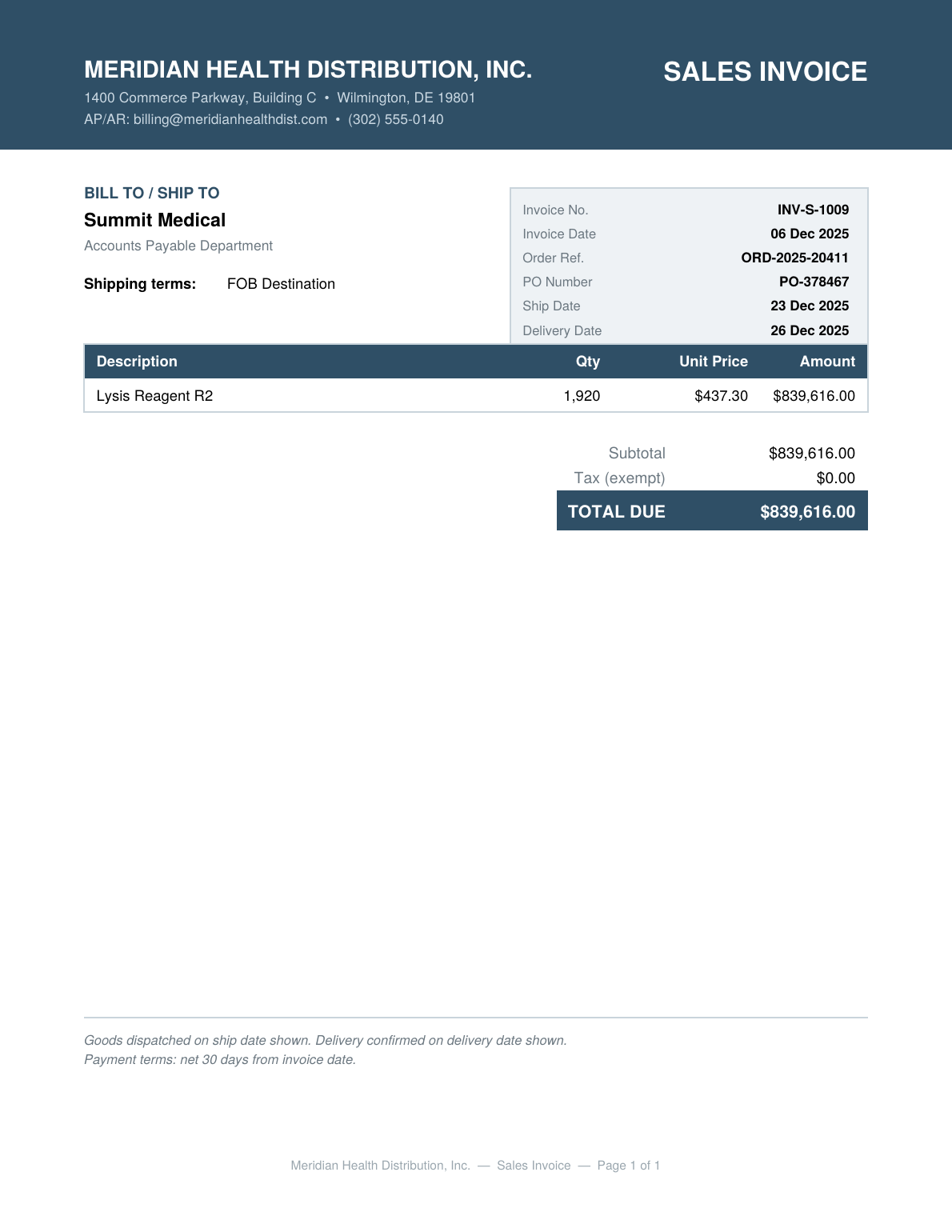

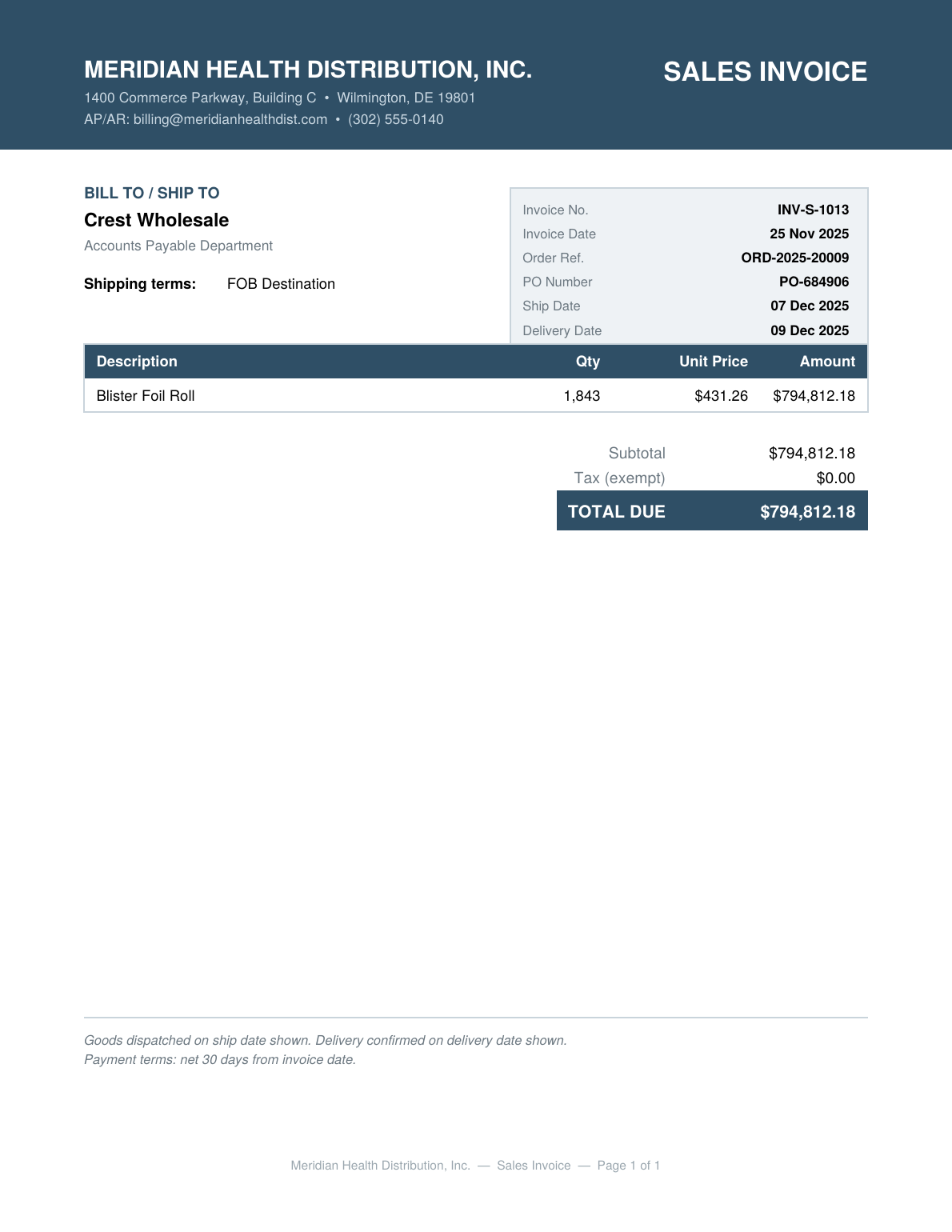

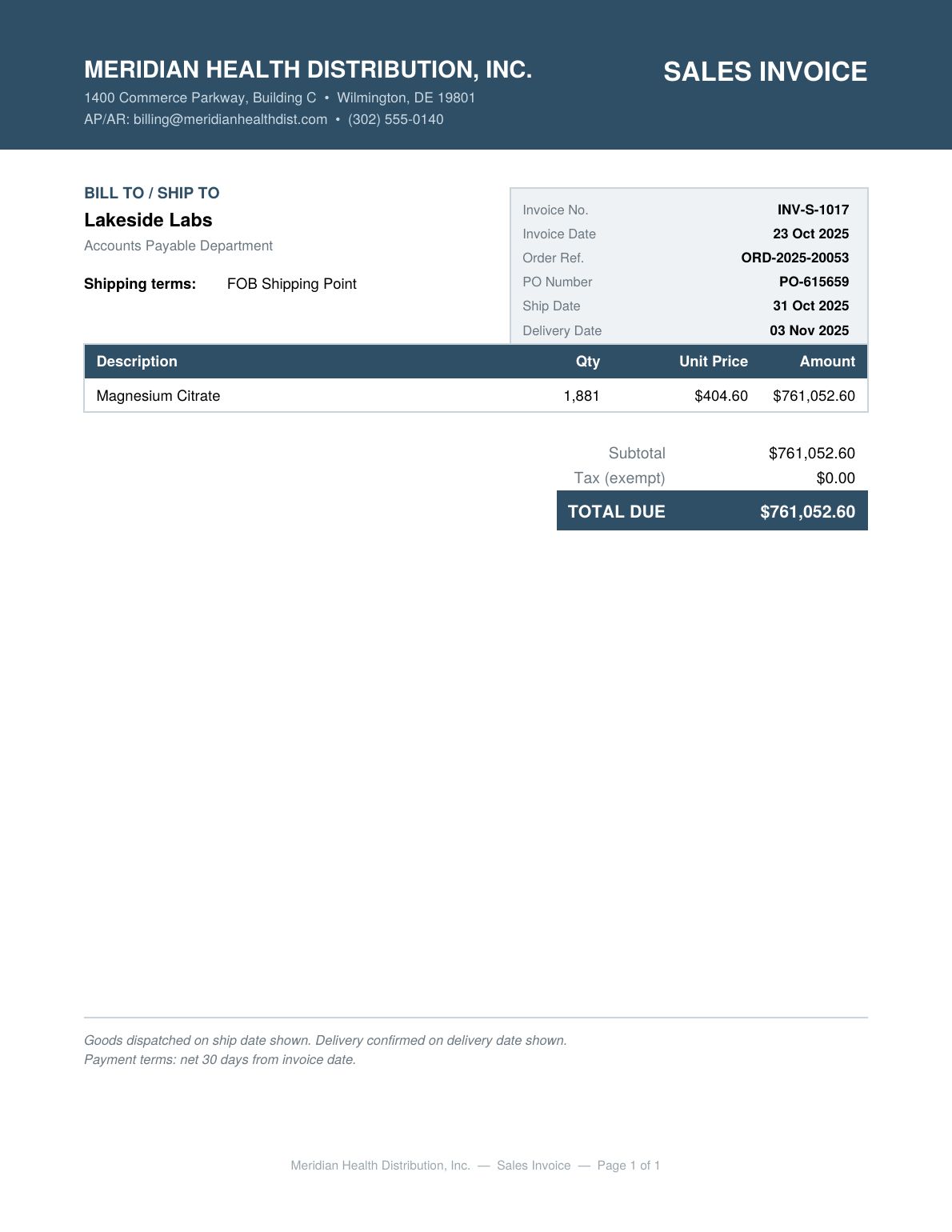

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

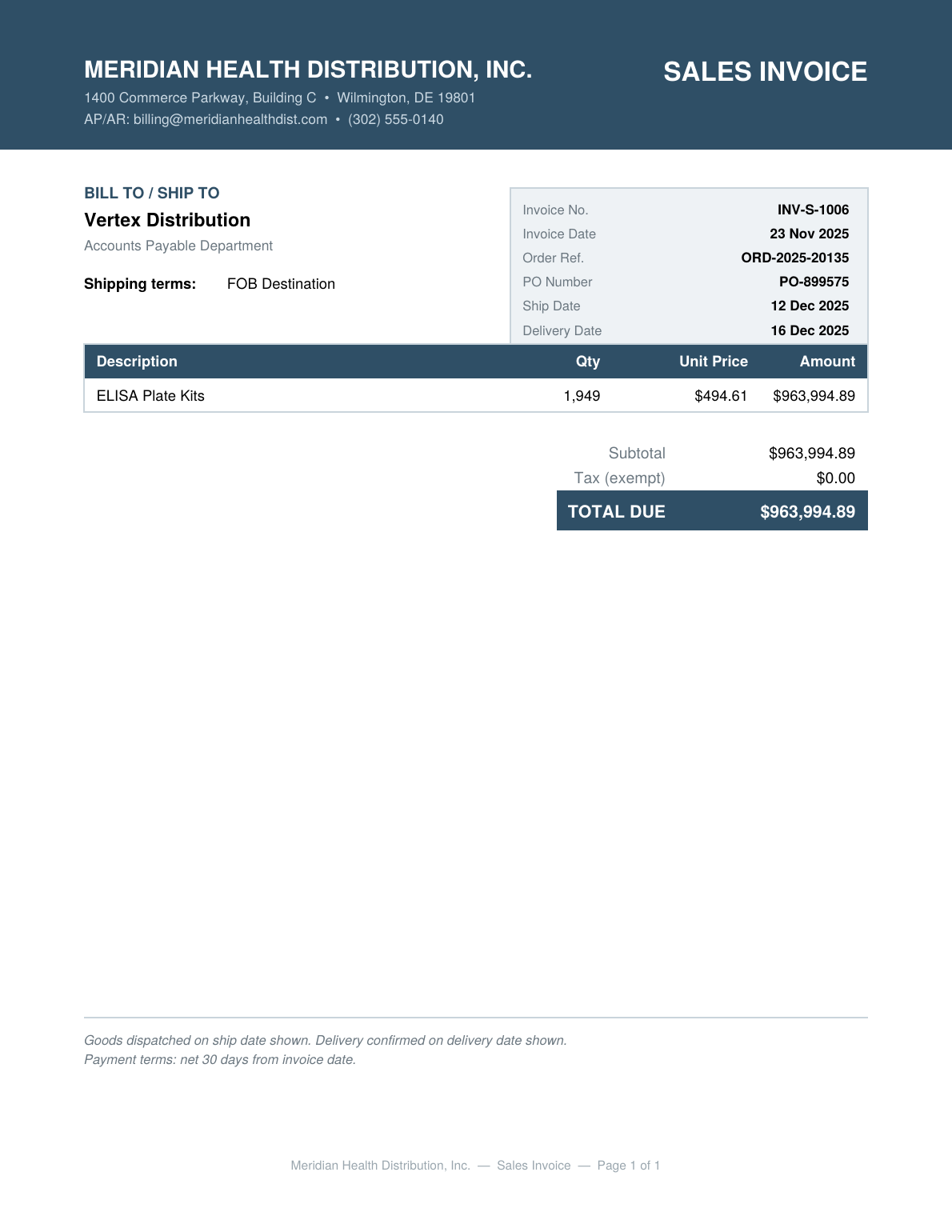

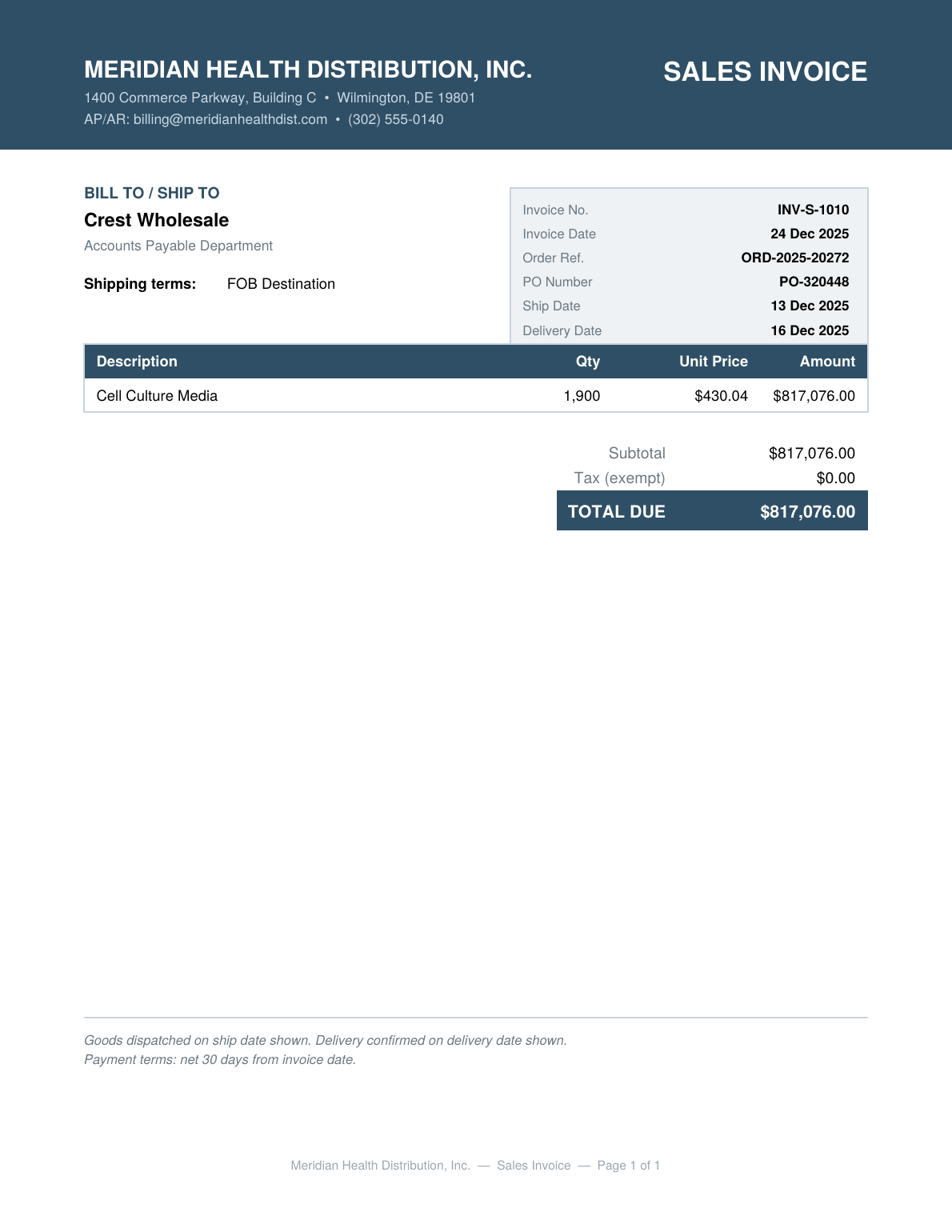

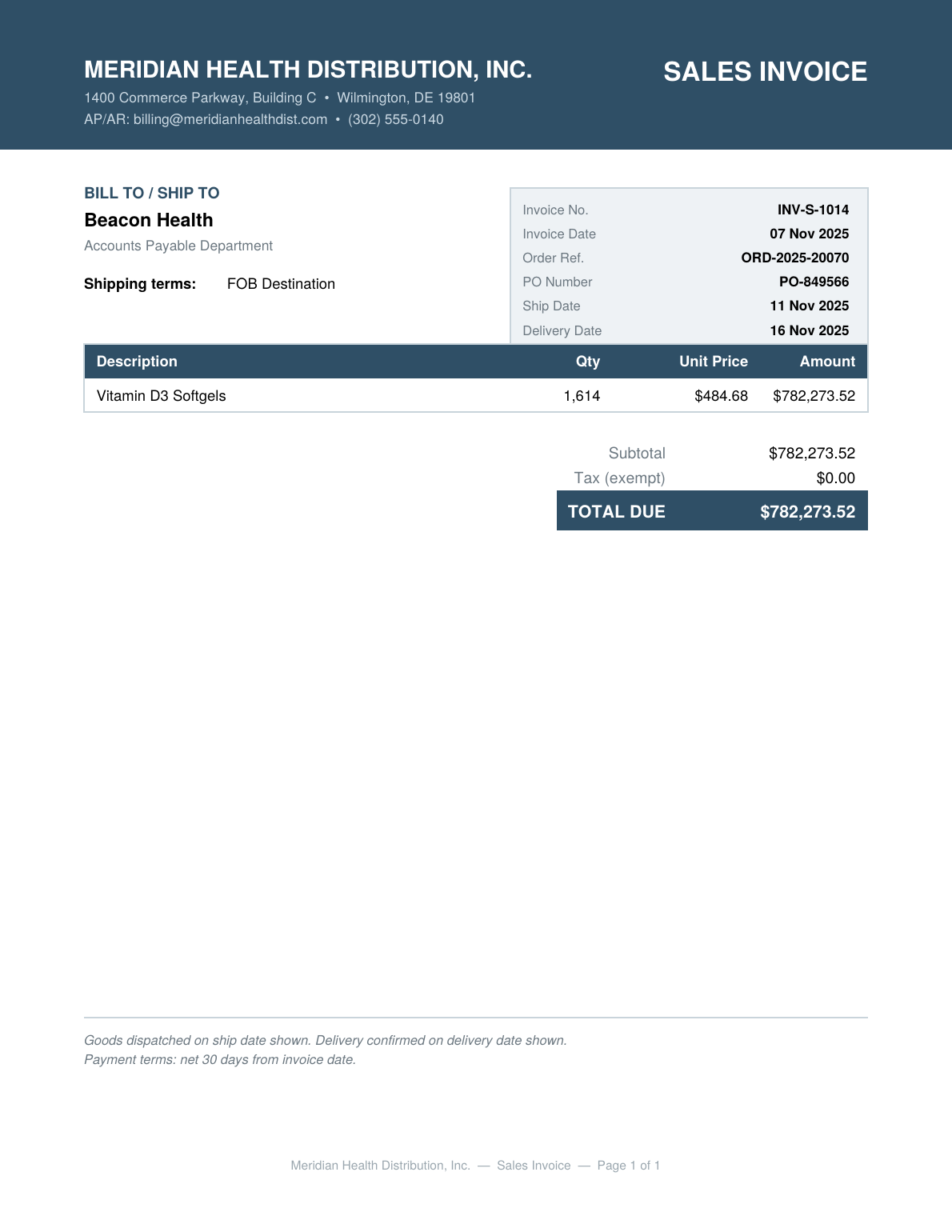

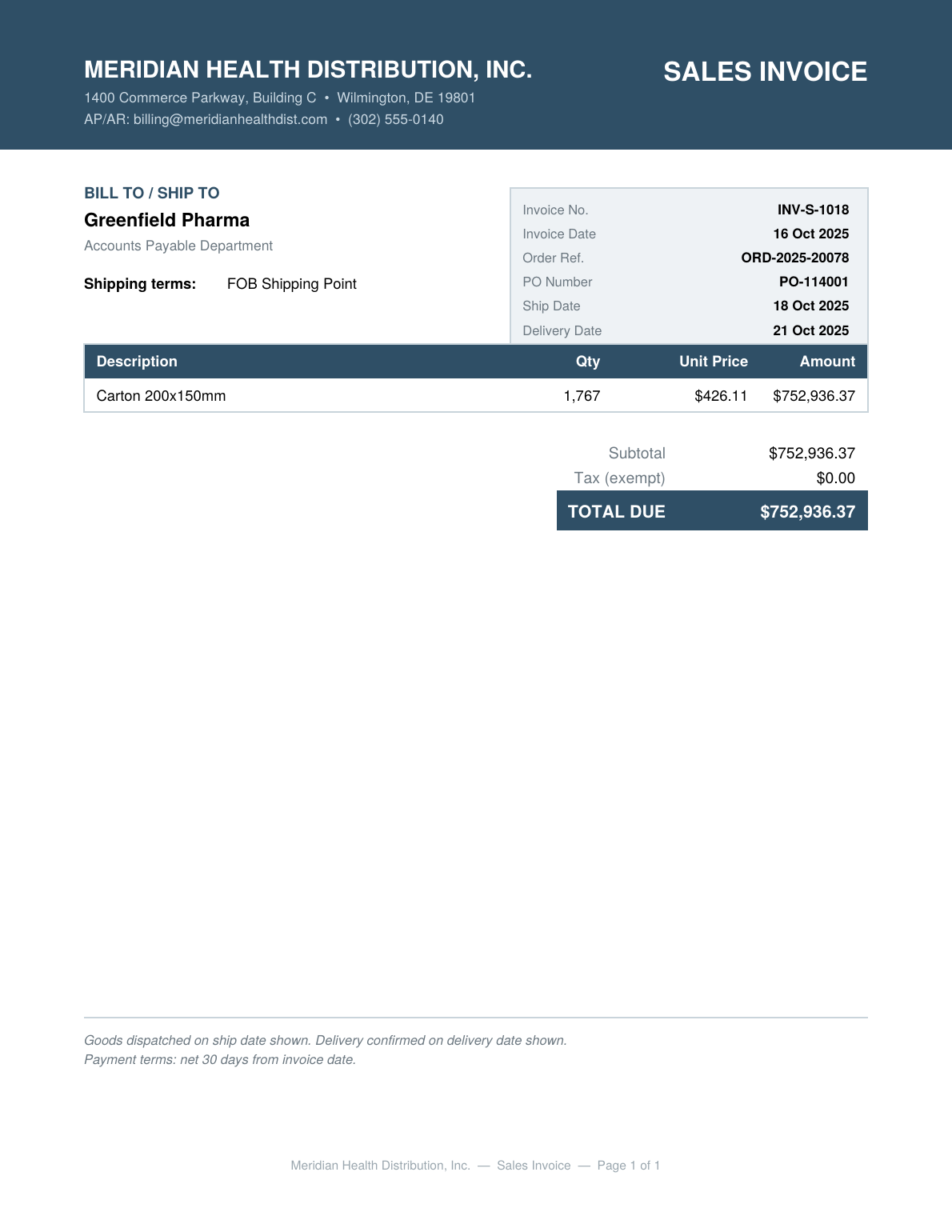

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

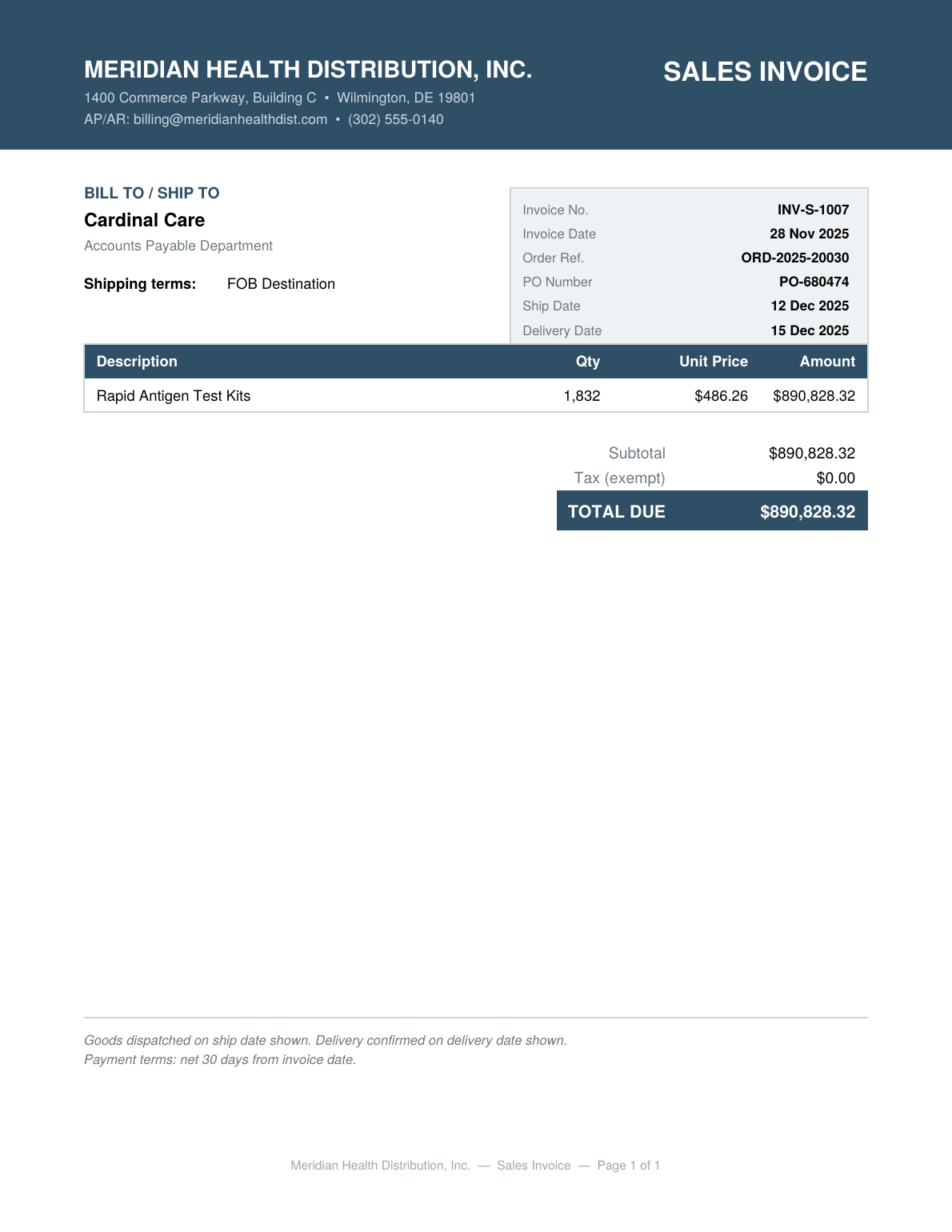

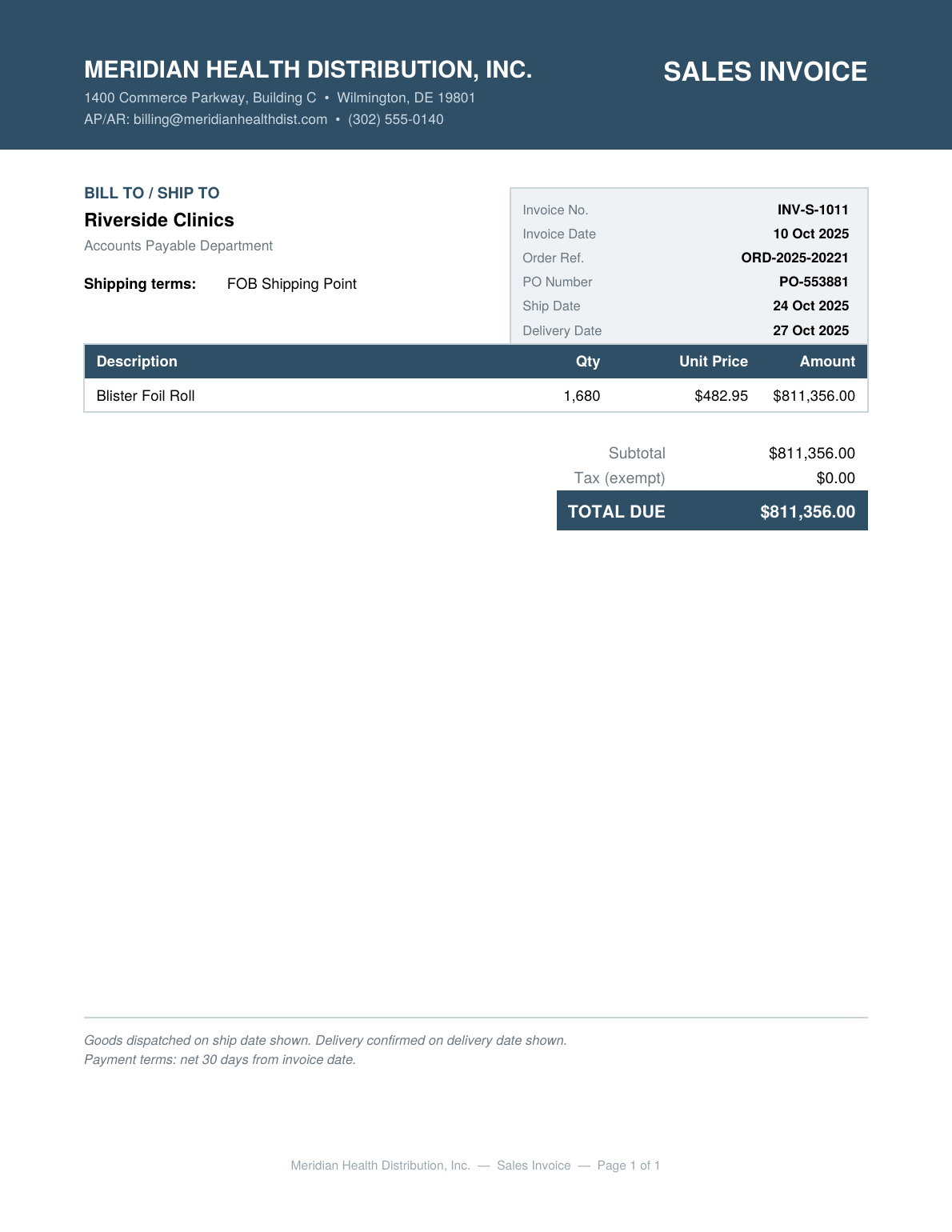

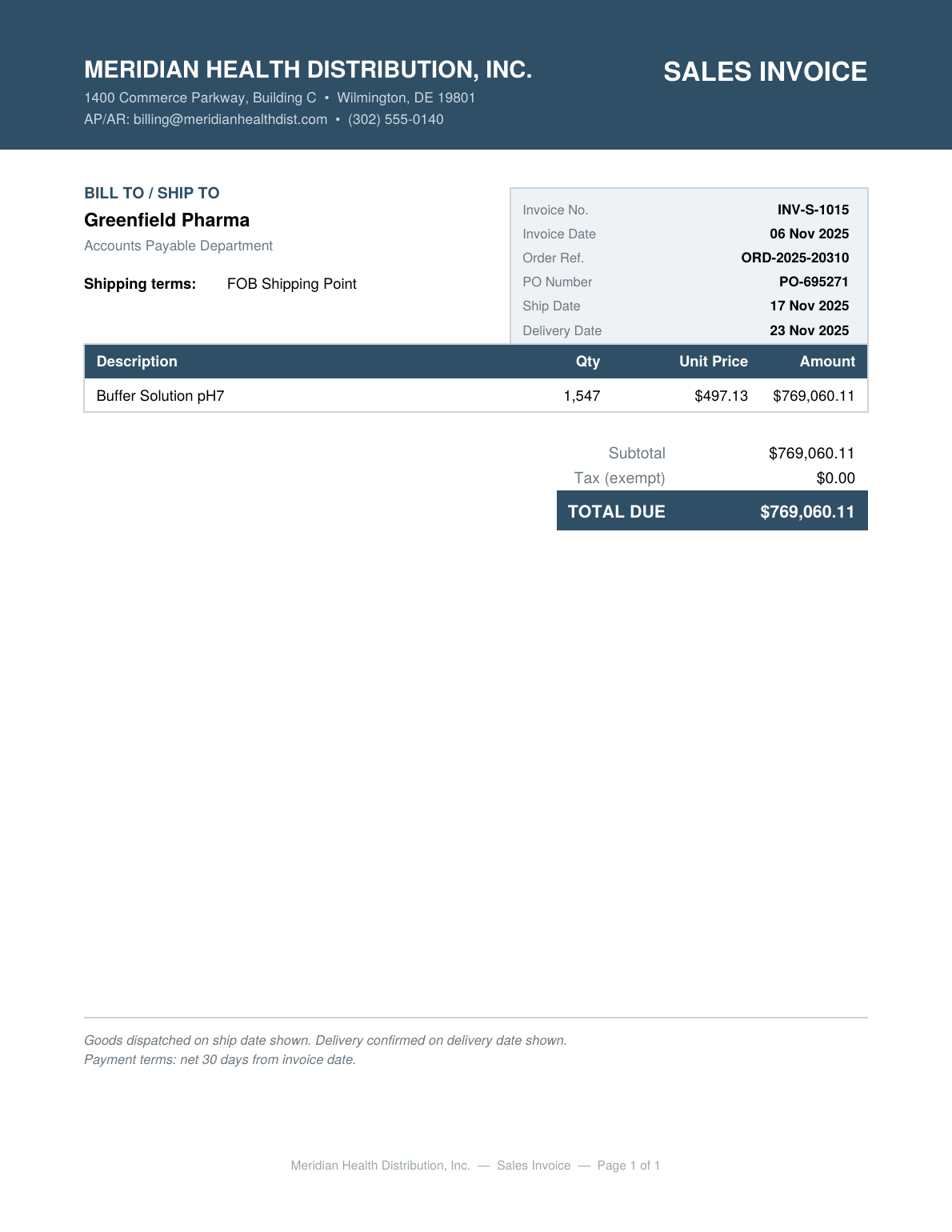

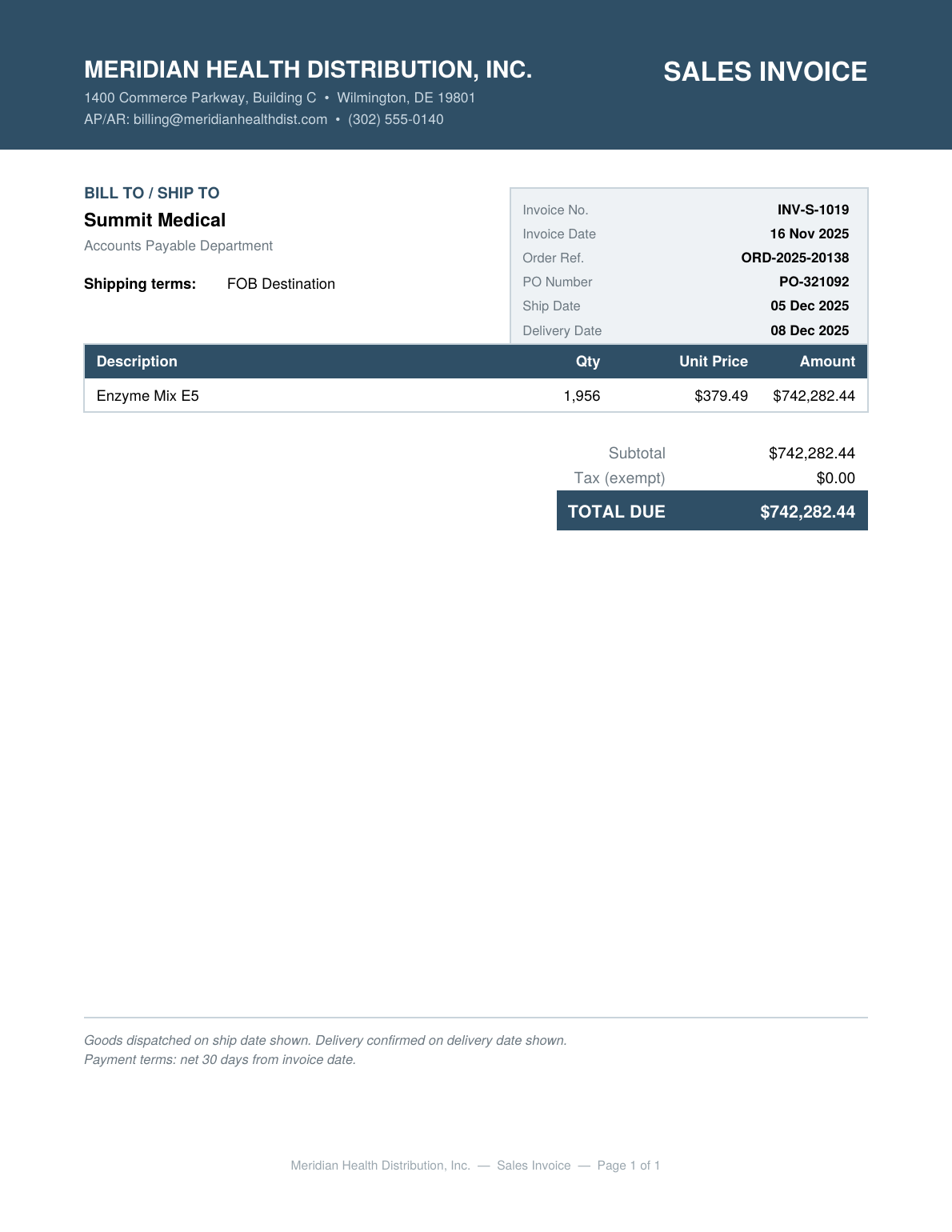

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

{kind=link}

expert_contributed — Author-generated; mirrors a vendor/sales invoice document image.

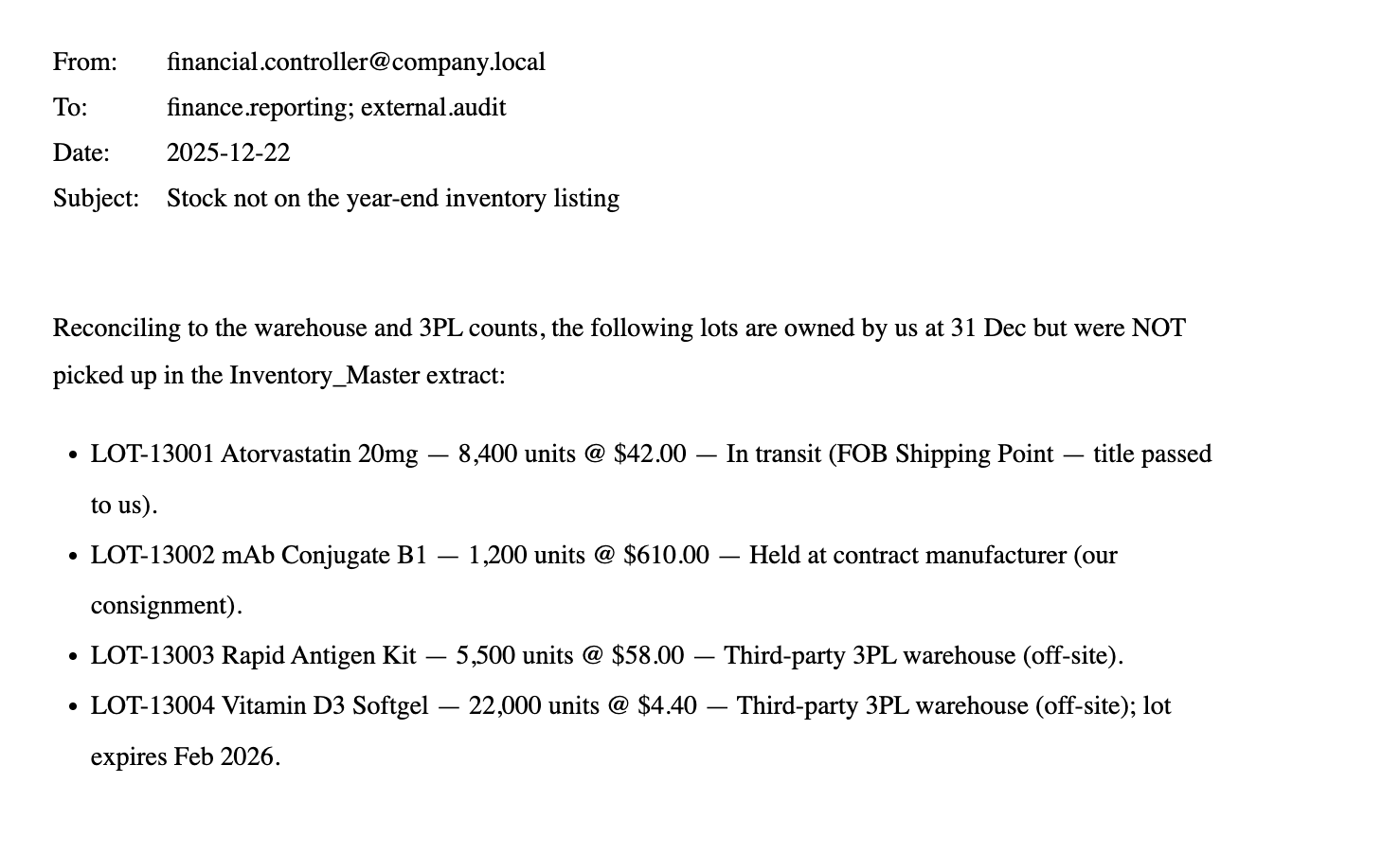

expert_contributed — Author-generated; mirrors a standard ERP inventory-master extract (lot, qty, cost, expiry, status).

expert_contributed — Author-generated; mirrors a company inventory operations manual / SOP.

expert_contributed — Author-generated; mirrors an order-log transactional extract.

expert_contributed — Author-generated; mirrors a shipping-log transactional extract.

expert_contributed — Author-generated; mirrors a vendor/system access-control entitlements export.

Gold Deliverables (2)

Download all (.zip)Gold Trajectory

Scoring Rubric

| ID | Criterion | Category | Pts |

|---|---|---|---|

| 1.1 | 4 exact-duplicate lots removed; 600 unique lots used | Calculation | 1.5 |

| 1.2 | Orphan shipment (ORD-2025-20503) excluded from revenue | Calculation | 1.5 |

| 1.3 | The 6 fully-unshipped Q4 orders carry no revenue | Calculation | 1.5 |

| 1.4 | Revenue computed on quantity shipped x unit price (not order value) | Calculation | 2 |

| 1.5 | Multi-line shipments reconcile to ordered quantity | Calculation | 1.5 |

| 1.6 | No over-shipments recognised | Calculation | 1 |

| 1.7 | All 13 emails accounted for; none silently dropped | Artefact completeness | 1 |

| ID | Criterion | Category | Pts |

|---|---|---|---|

| 2.1 | FOB Shipping Point lines recognised at ship date | Calculation | 2 |

| 2.2 | FOB Destination lines recognised at delivery date | Calculation | 2 |

| 2.3 | ORD-2025-20142 Q4 portion = $246,130.80 (1,329 units) | Calculation | 1 |

| 2.4 | ORD-2025-20142 deferred portion = $93,711.20 (506 units) | Calculation | 1 |

| 2.5 | 29-Dec FOB Shipping Point lines retained in Q4 | Calculation | 2 |

| 2.6 | 29-Dec FOB Destination lines (delivered Jan) deferred | Calculation | 2 |

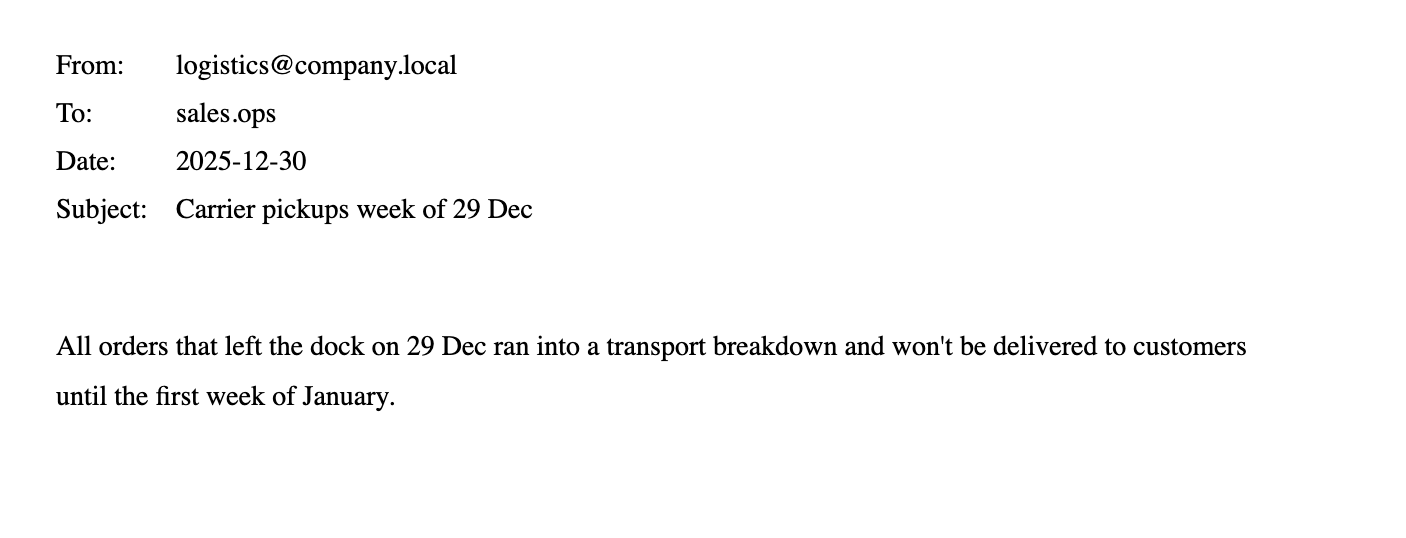

| 2.7 | SHP-70069 deferred to Q1 despite recorded 31-Dec delivery (per 2025-12-30 breakdown email) | Reasoning | 3 |

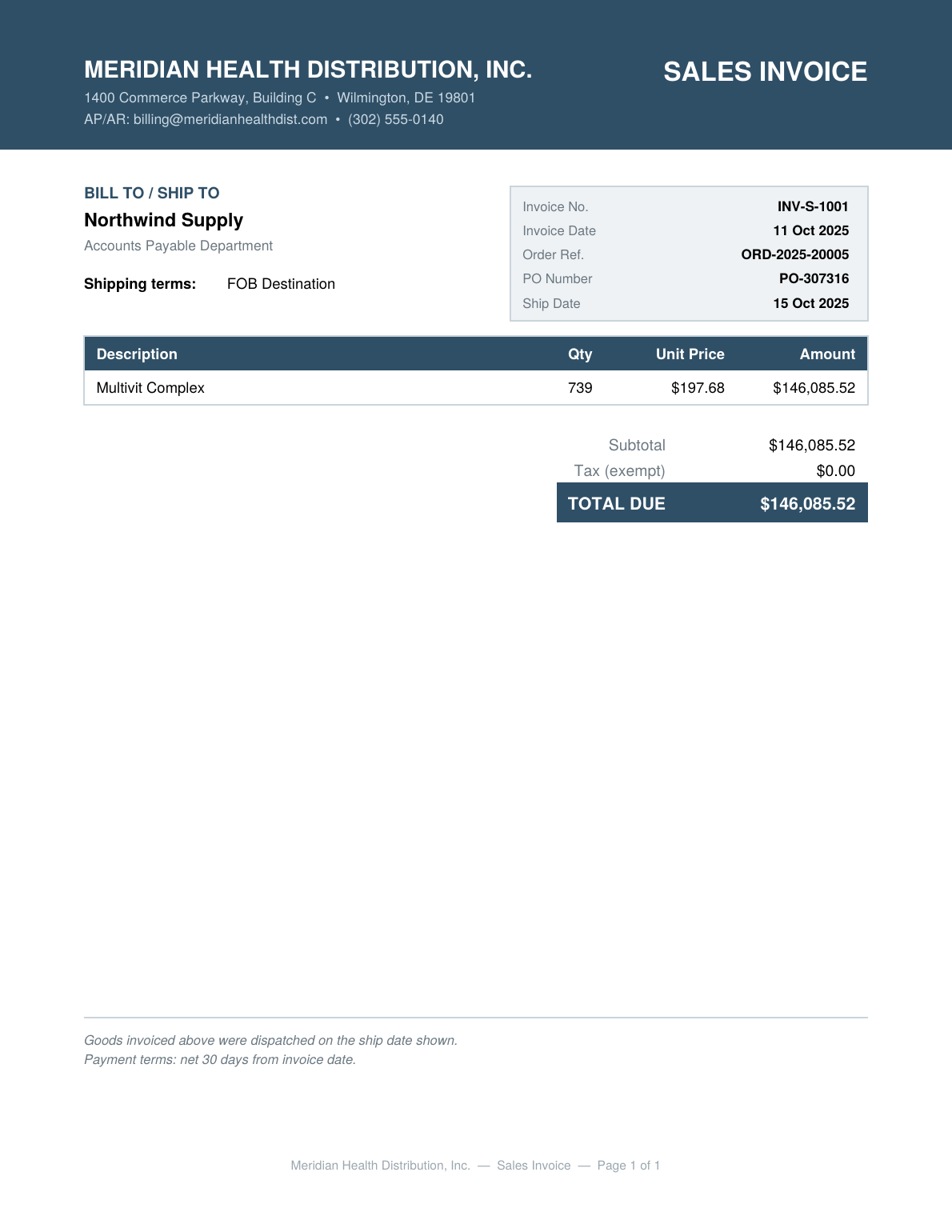

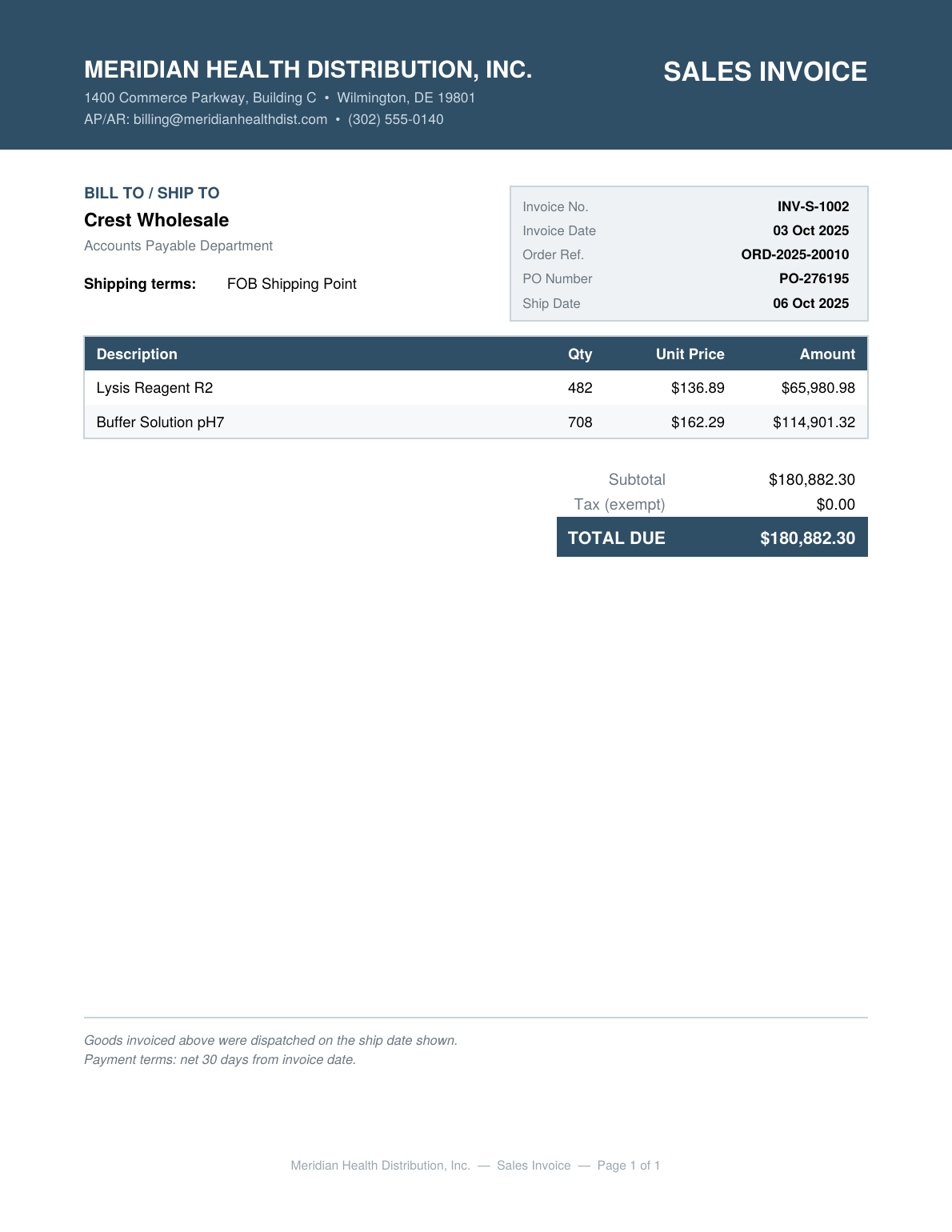

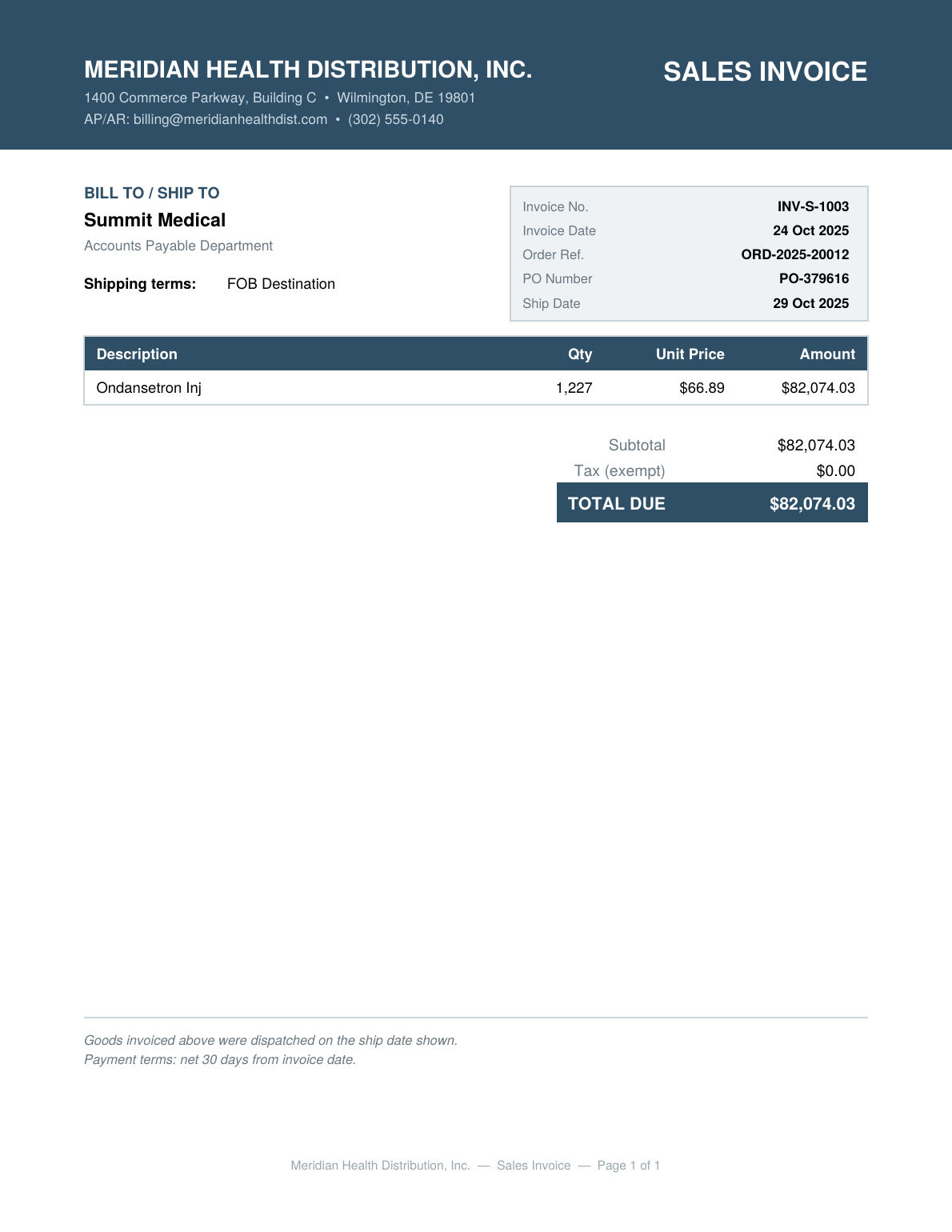

| 2.8 | The 4 invoice-only sales (INV-S-1001-1004) recognised in Q4, $542,283.74 | Calculation | 3 |

| 2.9 | 'Net 30 days' treated as a payment term, not a recognition trigger | Reasoning | 1 |

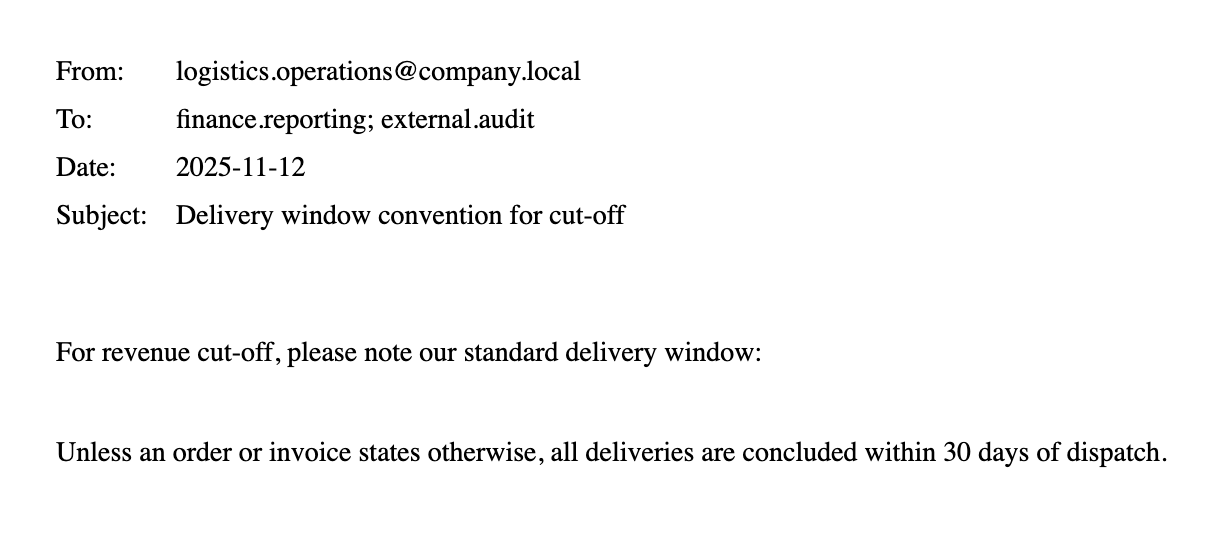

| 2.10 | 30-day delivery-window convention used to impute delivery where unstated | Reasoning | 1 |

| 2.11 | Stated Q4 revenue foots to the sum of Q4-tagged lines (consistency) | Artefact consistency | 1 |

| 2.12 | Stated deferred total foots to the sum of deferred-tagged lines (consistency) | Artefact consistency | 1 |

| 2.13 | FINAL Q4 2025 revenue = $120,047,883.16 (headline deliverable) | Calculation | 4 |

| 2.14 | FINAL revenue deferred to Q1 2026 = $4,492,129.21 (headline deliverable) | Calculation | 3 |

| ID | Criterion | Category | Pts |

|---|---|---|---|

| 3.1 | Gross warehouse extract (post-dedup) = $313,494,104.52 | Calculation | 1 |

| 3.2 | 3 recalled lots written off 100% = $677,448.18 | Calculation | 2 |

| 3.3 | Blank-expiry lots imputed via manufacture date + category shelf life (method) | Calculation | 1 |

| 3.4 | Reserve tiers applied: expired 100% / <=90d 50% / 91-180d 25% | Calculation | 2 |

| 3.5 | Expiry-reserve total = $13,783,218.29 | Calculation | 1 |

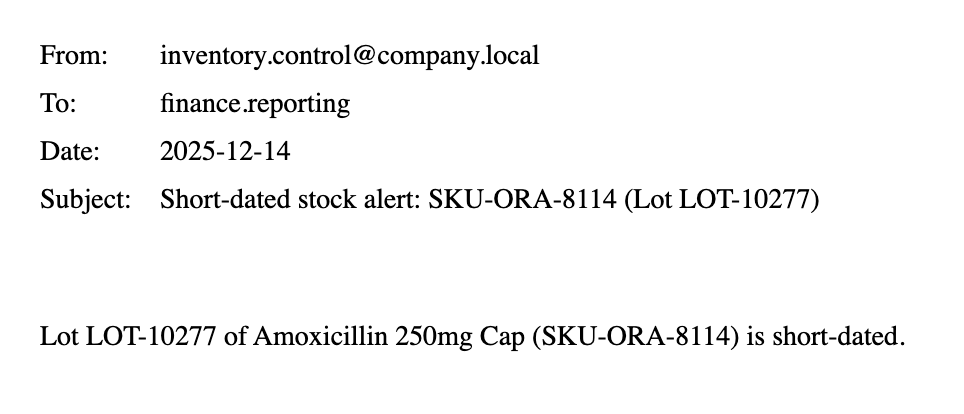

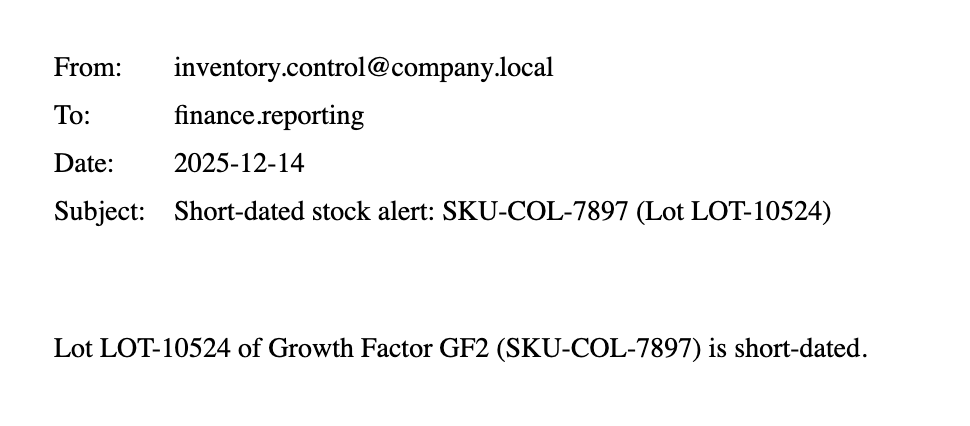

| 3.6 | 2025 short-dated lots (LOT-10277/10524) reserved 50% = $458,944.53 | Calculation | 2 |

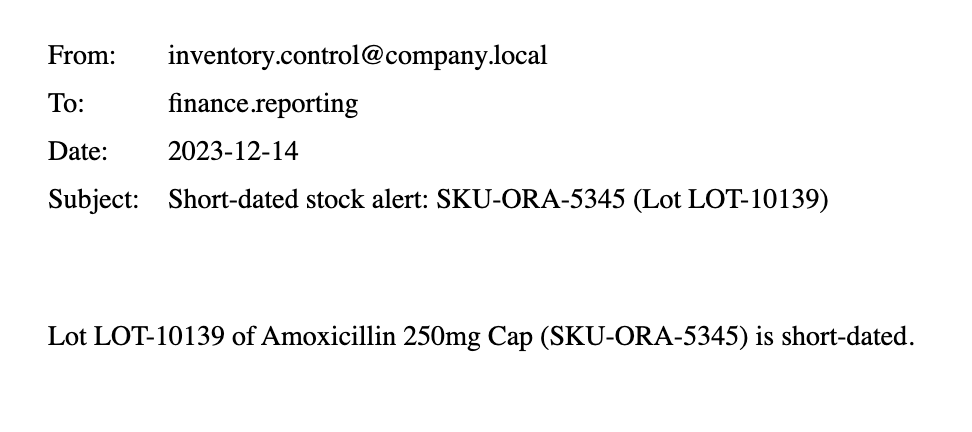

| 3.7 | Stale-2023 alert (LOT-10139, dated 2023-12-14) NOT treated as a current 50% short-dated item | Reasoning | 2 |

| 3.8 | LOT-10139 prudently reserved 100% ($881,540.88) and flagged as judgmental | Reasoning | 2 |

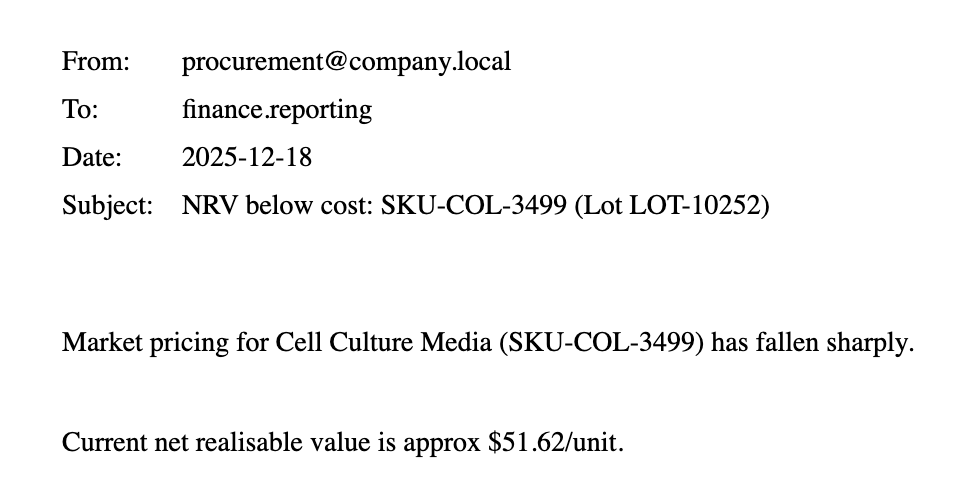

| 3.9 | LOT-10252 written down to NRV $51.62 | Calculation | 2 |

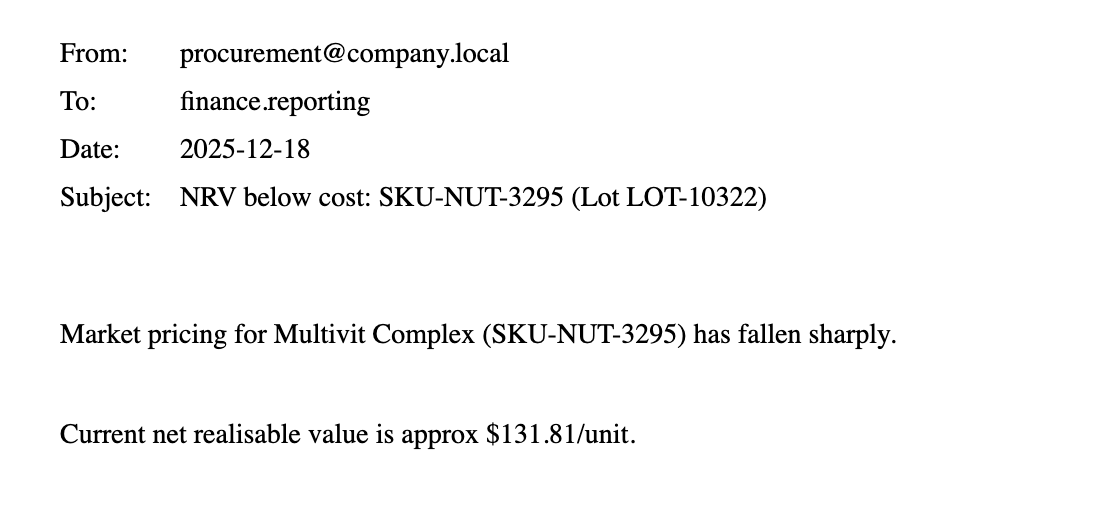

| 3.10 | LOT-10322 written down to NRV $131.81 | Calculation | 2 |

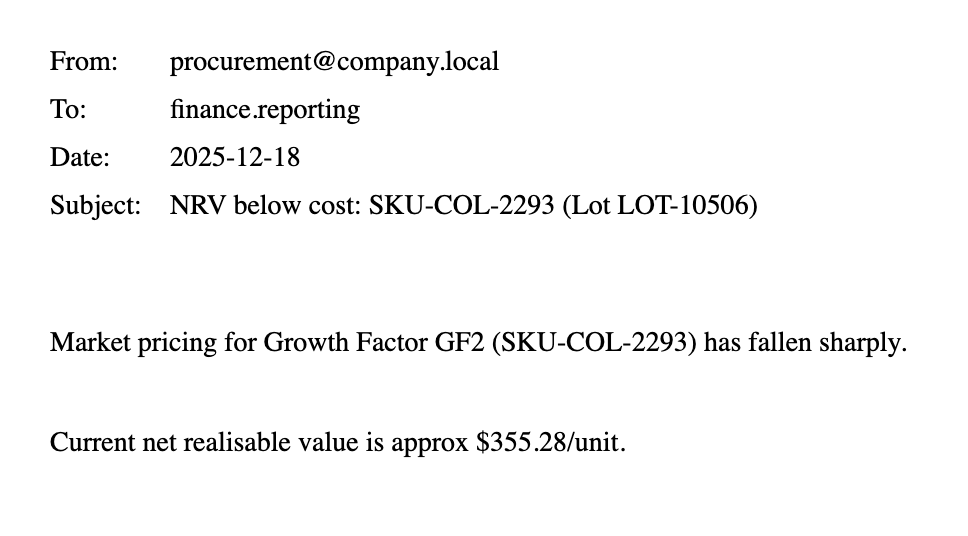

| 3.11 | LOT-10506 NOT written down (NRV $355.28 exceeds cost $310.57) | Reasoning | 3 |

| 3.12 | Packaging treated as non-expiring (no shelf-life reserve) | Reasoning | 1 |

| 3.13 | 12 in-transit FOB Destination lines added back at cost = $2,432,598.30 | Calculation | 2 |

| 3.14 | SHP-70069 additionally added to in-transit (+$28,797.00), 31-Dec date overridden | Reasoning | 1 |

| 3.15 | Email-13 four off-extract lots added at gross cost = $1,500,600.00 | Calculation | 1 |

| 3.16 | LOT-13004 (expires Feb 2026) 50% reserve applied (-$48,400.00) | Calculation | 1 |

| 3.17 | 3 sold-but-unrelieved lots (LOT-10076/10365/10450) removed = -$767,576.31 | Calculation | 2 |

| 3.18 | Stated net inventory foots to the build-up of the components above (consistency) | Artefact consistency | 1 |

| 3.19 | FINAL net inventory at 31 Dec 2025 = $299,953,175.23 (headline deliverable) | Calculation | 4 |

| ID | Criterion | Category | Pts |

|---|---|---|---|

| 4.1 | 20 of 58 distinct employees have >=1 SoD conflict | Calculation | 3 |

| 4.2 | 19 employees can both approve and initiate payments | Calculation | 3 |

| 4.3 | 2 employees can onboard a vendor and initiate payment | Calculation | 3 |

| 4.4 | EMP-1042 holds all three rights, across 3 fragmented provisioning records | Calculation | 3 |

| 4.5 | Ghost-employee / shared-bank-account test performed | Calculation | 1 |

| 4.6 | That Ghost-employee / shared-bank-account test's result reported as clean (explicit negative) | Reasoning | 2 |

| ID | Criterion | Category | Pts |

|---|---|---|---|

| 5.1 | Workbook is live-formula-driven (SUMIF/VLOOKUP/IF/SUMPRODUCT), not hardcoded | Format & integrity | 3 |

| 5.2 | Workbook recalculates with zero formula errors | Format & integrity | 2 |

| 5.3 | Figures tie across all workbook tabs (internal consistency) | Artefact consistency | 2 |

| 5.4 | Deck contains 5 core slides + cover + appendix | Artefact consistency | 1 |

| 5.5 | Each of the 3 headline numbers shows its consideration (qualitative basis) | Artefact completeness | 2 |

| 5.6 | Each of the 3 headline numbers shows its calculation (how derived) | Artefact completeness | 2 |

| 5.7 | Controls evaluation presented in the deck with priority remediation | Artefact completeness | 2 |

| 5.8 | Traps/exceptions summary delivered enumerating avoided pitfalls | Artefact completeness | 1 |